Table of Contents

Gen-Z nearly has everything they want to get in a single click. They are able to do anything without moving. They are able to do something without moving, anything is just as simple as clicking your phone.

Then, here’s a question

If improving technology would be a way of moving the industrial world to improve the world’s economy and job-working, then why do they hardly find a job? Why Gen Z are poor? Reaching 22,25 percent of jobless percentage across the Gen-Z population according to Kompas, they should have found a job in a click as they do in everyday life, right?

Now, it’s as simple as the environment works and forces. The answer to all of those would be in one sentence Gen-Z is designed to be Poor. Before you click the comment section and roast my statement, I’ll tell you how today’s life goes around us and how they crumble Gen-Z’s already poor behavior on finance.

Environments make Gen Z poor

The environment should include many aspects, but let’s delve into the economic aspect as it depends on Gen-Z’s jobless percentage. There are a lot of rising aspects in the environment, that dominantly shake and destroy our behavior on money-saving and job-working.

A. The rise of technology

I won’t count on many paying features that led to a wasteful style. We are growing in a state of gradually increasing technology. This rising technology has always been an integral part of our daily activities, whether we are a producer or consumers. This also led us to a different lifestyle from other generations.

Advertisement Receiving

Let’s see the differences. Back then, if people were going outside, they were likely to receive 1.000-2.000 advertisements per day.

Nowadays, those who stay at home, are likely to receive much more advertisements per day. If we go outside, 6.000 advertisements are likely to be met. In conclusion, people would be likely to be attracted to buy things as they receive much more advertisements.

Maybe, the previous generations have to think wisely about managing their savings, but how about the young generations? that has always been ingrained with too much attractions since little.

If people nowadays are able to receive much advertisements when not going outside, we know that the Internet and social media are the impostors.

100 years ago, people may have known about products either from mouth to mouth or in newspapers. Mouth-to-mouth includes relations and much tiring walking around. Newspapers also need much of a payment.

Additionally, if we’re talking 90 years ago, we were faced with the great depression, a long-lasting history of economic downfall. Therefore, we know how much people struggled to promote their products back then.

Products’ Introduction

Now, look at us, scrolling 2 times you will get two advertisements. With loaded information on a page, you are able to be attracted to a product easily from across the globe. Walking around the town, you meet another advertisement on a big screen in a building with a much more attractive advertisement. Therefore, how doesn’t that make Gen Z poor? you will meet at least 10 ads every day.

Payments in ease

Card payments, mobile wallets, QRIS payment, Cash On Delivery, Buy Now Pay Later, etc. Those payment methods, whether you know or not, have been make Gen Z poor as companies scratches their savings.

As we don’t have to bring money to shop anymore, we are only making ourselves rotted up with shopping features that makes us have less credit history.

According to an April 2022 LendingTree poll, a significant 43 percent of Americans reported using a Buy Now, Pay Later (BNPL) service, a notable increase from 31 percent in 2021. These services are especially popular among women, members of Gen Z (ages 18 to 25), and individuals earning between $50,000 and $74,999 annually.

B. The Rise of Childishness

Sign in to your social account now and see what’s trending right now. You may occasionally find some people in their mid-20s acting like a child. Or maybe you may see some fandom screaming in tantrums and crying like a toddler as their favorite celebrity makes its view to them. Besides that, we may see the other proofs of childishness, which sadly isn’t only on social media.

Over healing

Self-healing is beneficial for your mental. I’m not blaming Gen-Z for healing, I’m certainly blaming them for overdoing it. I recommend you heal yourself after certain hard times, but It’s bad when your brain starts to associate it with “overspending as much as I want”.

It’s a bias that you need healing every time you go home after work (especially if you want to save money). It’s also a mistake if you have to do it when you feel a little stressed. These mindsets make Gen Z poor and poorer.

Back then, people face many harsh experiences through war and any other tragedies. In fact, toddlers were assigned to do harsh work, either to receive money or a slave. Some of the most popular one would be working as a chimney cleaner or a heaver.

Not only that, in the 60s-90s, students were studied by “killer” teachers. If you told your parents that your ear got pinched, your parents would get mad back at you as you were being an inobedient. Those experiences lead to mental development that is highly beneficial in working life.

Undeveloped mentality

Presently, our environment has been changing. Once, your teacher will get mad, and your parents will shout back to the teacher for being a little too harsh.

Afterward, you’ll experience a very huge culture shock in working life. This phenomenon is also the result of job hopping on Gen Z. In fact, according to a September 2023 report from ResumeLab, 83% of Gen Z workers consider themselves job hoppers.

Nevertheless, job hopping could lead to financial instability as you possibly experience unemployment between jobs. There are still many disadvantages for being job hopper. Although hopping one job to another occasionally may seem fine to certain conditions, you can’t quit job just because you don’t like something. In the end, no company wants their employee has a weak mentality.

C. The rise of extravagant lifestyle

Keeping Expectation

As a person who sometimes struggles with friendship, I know what it feels like to maintain others’ expectations.

Unfortunately, those friends that demand your high social picture would only lead you to bad money management. In fact, according to a recent survey, more than a third (36 percent) of Gen Z stay poor as they maintain friendships with friends who encourage them to spend expenses too much.

Reporting from era. id, the misalignment of financial priorities between Gen Z causes the breakdown of friendships and encourages a phenomenon known as FOMO. The Credit Karma Institute survey stated that 76 percent of Gen Z are in debt due to FOMO behavior, which is a dangerous consequence. In conclusion, spending the last money you have on demanding friends isn’t something worth doing.

Keeping them up to date

Can you count how many social media trends that involve anything expensive? According to survey data, 82.5 percent of respondents regarding this issue said that teenagers always follow existing trends without looking at any motive. This causes them to buy an item spontaneously without having to plan it.

Many teenagers express that they follow those unnecessary trends because they think it’s necessary to express themselves and as a differentiator of identity.

Wanting to Boast

Another social media stereotype that has been engraving us, is flexing. This flexing phenomenon emerged from a group of people who were pushed to gain recognition. This has become increasingly widespread since the number of groups of people who call themselves “crazy rich” has increased. Like the general boastful people, they show off expensive items. These so-called crazy rich try to continue to exist through their social media.

The act of flexing cannot be separated from actions of showing off one’s assets on social media. This action can take the form of showing off account balances and luxury items.

Sadly, this has been affecting many people, mainly Gen Z, who in everyday life consume this type of content. These flexing things will disrupt your financial condition as you always follow your desires in fulfilling your habit of showing off. It’s as if there has to be something new to show every day.

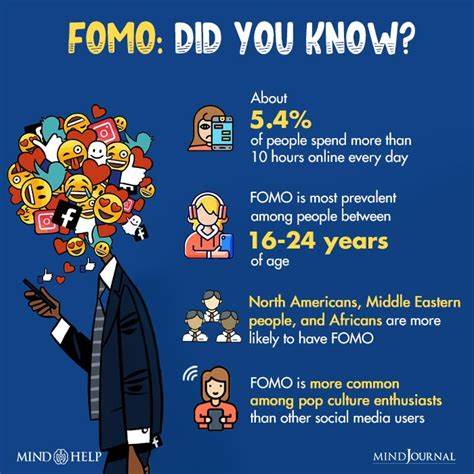

D. The Rise of Soft Saving

According to Deloitte’s 2023 Annual Gen Z and Millennial Survey, which included 22,000 respondents from 44 countries, it was revealed that one in five (20 percent) Gen Z individuals spend five or more hours a day on social media platforms, while 17 percent of Millennials spend five or more hours a day watching videos.

What will happen?

Now, the outcome, as we expected could be highly extensive. The combination of those produces concerns for future economic well-being, which would connect the other aspects.

As Gen-Z transitions into adulthood, many lack essential knowledge in budgeting, saving, and investing, while simultaneously being influenced by a culture that promotes excessive spending. If these persist, the consequences could extend beyond Gen-Z being widely poor.

Bad Financial Stability

The rising prices and lower money-saving (soft-saving) should be the main aspects of financial instability. Gen-Z rarely care how many digits they have in their bank accounts. Gen-Z also hasn’t been able to act mature regarding utilizing their money-using. Besides that, our behavior on money, which overall overuse it, isn’t factored only from ourselves, but also how our environment has been going.

We can’t get out of the fact that our surroundings also have been a huge aspect of our savings. For instance, technology has ingrained us with thousands of persuasive ads and features.

If you don’t have any social media, then you can turn on your TV or go outside and count how many unique advertisements you can find. Additionally, there are fluctuating inflation, raging wars, economic crises, and many others that make Gen-Z poor and poorer.

Working Instability

One of the most crucial reason for “Gen Z poor” is their immaturity and idealistic mindset. While previous generations are resilient in working life due to the childhood “harsher” environment, 50% of Gen-Z don’t approve of working with certain companies that don’t involve “Social Justice”, making them Social Justice Warrior.

Many Gen-Zeers also desire flexible work options and work-life balance, and they’ll leave their jobs without it.

As BBC (in its photo) interprets it, Gen-Z also called the workers who want it all, Work-life balance, fair pay, and value alignment: today’s youngest workers want it all – and are willing to walk away if they don’t get it. These factors also lead them to job-hopping.

Unfortunately, while job hopping is recorded to increase employees’ salaries by 28%, this action leaves them with Inconsistent experience, job dissatisfaction, and sometimes difficulty in finding a job between jobs. All of those components leave employers with biased feelings toward this generation and therefore, occasionally reject them upon age.

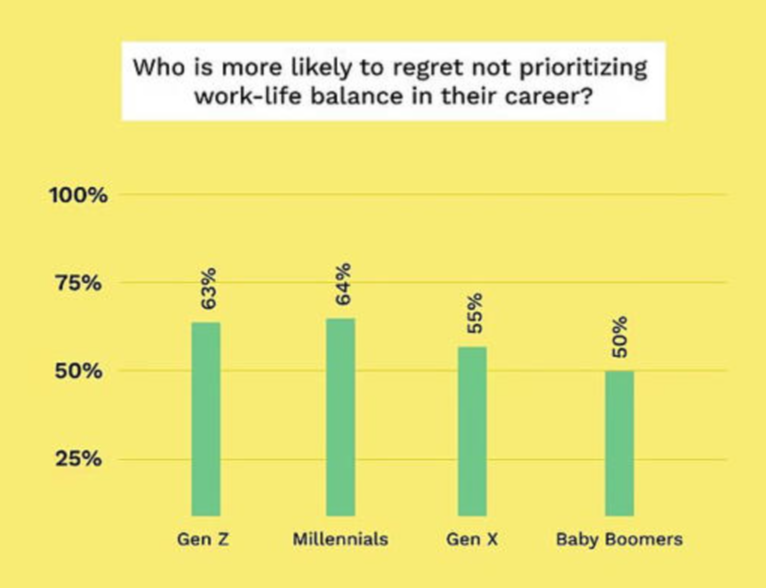

Higher Percentage of Financial Regret

In the end, they regret what they were doing. The percentage of financial regret could be different due to different factors, the factors could be failure to work-prioritize, regret of starting a new job, not investing sooner, regret of being a person with Fear of Missing Out (FOMO), etc. These regrets could affect them poorly, in mental health for instance.

According to a recent Bankrate survey, 60% Gen Zeers experience financial regret and it’s stressing them out more in 2023 than in 2022, compared to just 45% of Gen Xers and 38% of baby boomers.

It’s also reported by MSN that 59% of Gen Zeers failed to prioritize their work-life. Besides that, according to a January survey conducted by The Muse, which included over 2,500 Millennial and Gen Z jobseekers, about 72% reported experiencing surprise or regret after starting a new job, finding that the role or company was significantly different from what they had been led to believe.

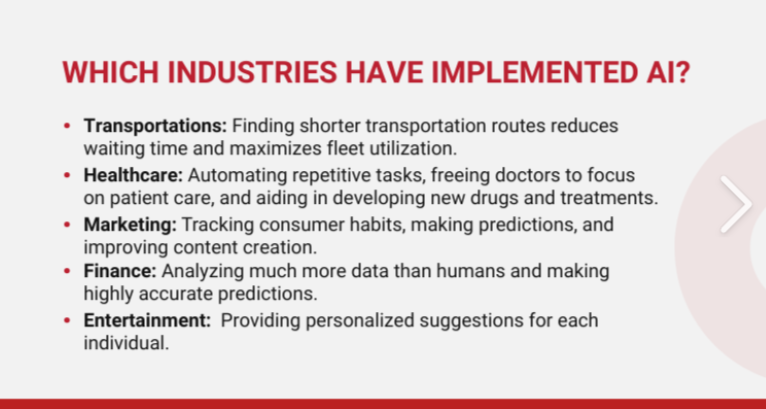

Loss to AI

It’s widely known that Artificial Intelligence would replace humans on specific jobs as they win over humans in several aspects. AI effectively automates repetitive and routine tasks, which means higher efficiency than humans.

AI systems are also able to perform tasks with high accuracy. This benefit of AI makes them a more valuable asset than humans, specifically in industries with critical accuracy. And, what’s the most important for all sectors is that AI will be highly more cost-effective than humans as they demand revenues and salaries. AI is also able to work continuously without breaks, vacations, or wages.

The negative news for humans, people will be widely unemployed, particularly in industries where routine, repetitive tasks are common. This change could intensify economic inequality, leaving many workers struggling to adapt. Ethical concerns also emerge, especially regarding biases in AI decision-making and the potential loss of human connection in services increasingly dependent on automation.

How to have a good relationship with money

A. Orchestrating into mindful spending habits

Mindful spending is the practice of making intentional and conscious choices when it comes to your financial decisions. It involves aligning your spending habits with your values, priorities, and long-term goals, an approach to managing our finances that goes beyond simply tracking expenses and saving money.

It is about developing a deep awareness of how our financial choices affect our overall well-being and aligning those choices with our values and long-term goals.

By being mindful of our expenses and consciously choosing where to allocate our financial resources, we can prevent the accumulation of debt that often comes from impulsive or excessive spending.

Mindful spending encourages us to consider whether a purchase is truly necessary and whether it aligns with our values and long-term financial goals before making a decision.

Here’s an example, you went into Balenciaga and found a navy leather work bag. You really want this bag, but you know you are on saving mode today. Now, you have to set your mindset into a mindful spending.

- Think about why you really want this bag

Pausing to think your aim on buying this bag is a helpful and healthy addition to learning to spend mindfully. Trying to evaluate the reasoning behind a purchase is critical. - Ask yourself if you need it

Ask yourself why you need it. You talk to your inner-self and your mind answers that you like it. If the answers you got are not urgent or necessary, you should have known that you don’t need them in the first place. - Why do you want to save money

You know you can’t buy it, but your heart leaps to you and gives you vision that you will get showered with compliments, praises, etc if you buy this bag. Now, talk again to your inner-self back, why do you want to save? is it because you want to give something to your loved ones as a present? or you want to buy a house? - Which one is more worth it?

If you know why you want to save money, ask yourself which decision you think will be the most worth it. At this point, you should know your priority. Step out of the shop and get back home.

B. Set Clear Financial Goals

However, people’s needs for money and the aim of savings are relatively different. Therefore, people set a specific goal on a specific duration of saving.

- Short-Term Goal: Save $1,000 within the next six months to build an emergency fund for unexpected expenses like car repairs or medical bills.

- Medium-Term Goal: Pay off $5,000 in credit card debt within the next year to reduce interest payments and improve your credit score.

- Long-Term Goal: Save $20,000 over the next five years for a down payment on a house.

C. Educate on the Power of Compound Interest

Now, to save money, you might be attracted to adding your savings with investing. As JL Collins explains in his book The Simple Path to Wealth, Compound interest defines the interest you get from interest, that’s why it’s called interest on the interest”.

Compound interest is calculated on the principal amount and the accumulated interest of previous periods. Understanding how compound interest works can motivate Gen Z to prioritize saving and investing over spending.

For calculating your compound interest you can count on a calculator from the US government.

D. Promote a Growth Mindset Over Materialism

In fact, the poor mindset of Gen Z is one of the many reasons Gen Z doesn’t get rich and stay poor, even poorer. By valuing experiences, learning, and growth, they can shift their focus from accumulating things to building a fulfilling and financially secure life.

Besides that, in the book The New Psychology of Success by Carol Dweck, she explains that a growth mindset encourages continuous learning and personal development, rather than focusing on materialistic personality as a measure of success.

By studying the concept of a growth mindset, we will get guidance for career and financial success, emphasizing learning, effort, and resilience over the pursuit of material wealth. Examples of improving your mindset could be;

- Taking small steps each day toward your goals.

- Getting out of your comfort zone.

- Rolling with the punches.

- Seeking out new perspectives.

- Believing that failure is a learning experience.

E. Challenge Social Media Influences

To handle the pressures of social media and keep your finances in check, embracing digital minimalism can be highly effective. This means intentionally cutting down on social media use and focusing only on content that genuinely benefits you. By curating your feed to follow accounts that align with your values and financial goals, you can avoid the trap of impulsive spending.

Practicing mindful consumption—by questioning whether a purchase truly fits your long-term goals—can help you make more deliberate choices. Understanding how social media algorithms work allows you to critically assess what you see and set limits on your usage. These steps can help you maintain better financial health, improve your well-being, and encourage personal growth by reducing the influence of fleeting trends and superficial pressures.

Therefore, we could implement some examples like;

- Limit Social Media Usage

- Unfollow influencers who post unnecessary things.

- Set Boundaries by tracking your social media’s screen time.

F. Enhancing Financial Literate

Financial Literacy means one’s understanding of money topics, such as budgeting, investing, saving, and many others. Not everyone knows that Financial Literacy is highly essential in everyday life as it could lead to many pitfalls for one who doesn’t have knowledge of it. Being Financially illiterate could lead to many negative consequences, such as poor spending decisions, lack of saving preparation, and lack of financial emergencies.

Furthermore, Robert Kiyosaki emphasizes the importance of having a high Financial Literate in his famous book Rich Dad Poor Dad. He emphasizes its importance as a key component of achieving financial success and independence. There are some important points regarding financial literate on his book;

1. Understanding Money

Financial literacy involves understanding how money works, including concepts such as investing, asset management, and financial statements. It’s not just about earning a paycheck but about making money work.

2. The Importance of Its Education

Kiyosaki argues that acquiring financial education through books, courses, and mentors is crucial for financial success as he expresses that traditional education focuses only on academics, not with practical.

3. The Importance of Financial Independence

Financial Independence means building multiple streams of income and not relying solely on a paycheck from a job. For instances doing investments and establishing businesses.

4. Overcoming Fear and Taking Risks

Kiyosaki explains in his book that his rich dad encouraged him to invest in real estate without the fear of losing money (although Kiyosaki was actually afraid).

In continuation, he argues on his book that financial education helps people understand risks and make informed decisions, rather than being paralyzed by fear.

5. The Big Role of Entrepreneurship

Entrepreneurship and investing are highlighted as pathways to financial success. Kiyosaki believes that understanding how to create and manage a business is a valuable aspect of financial literacy.

He also references the benefits of starting and running a business as a means to achieve financial freedom and build wealth.

Home Blog

Sources

https://www.investopedia.com/articles/investing/020614/learn-simple-and-compound-interest.asp

https://www.investopedia.com/terms/f/financial-literacy.asp

https://personalfinanceblogs.com/mindful-spending

https://www.apartmenttherapy.com/mindful-spending-ideas-37233799

https://www.bbc.com/worklife/article/20220613-gen-z-the-workers-who-want-it-all

https://www.shafiq.id/berita/187/bahaya-flexing-atau-suka-pamer-di-media-sosial/baca

https://www.kompas.id/baca/english/2024/05/20/en-mengatasi-pengangguran-gen-z

https://www.cnbc.com/2022/09/13/understanding-the-risks-of-buy-now-pay-later-apps.html